Update on Section 301 Tariffs, List 4

Update on Section 301 Tariffs, List 4

Details on Section 301 Imports from China

Information derived from U.S. Customs and Border Protection Cargo Systems Messaging Service #39587690 on August 30, 2019.

This messages provides notice of modification to the action being taken in the Section 301 investigation which increases the rate of additional duty from 10 to 15 percent for the products of China covered by the $300 billion tariff action (Tranche 4) published on August 20, 2019.

Background

In August 2019, the United States Trade Representative (USTR) introduced another imposition of additional tariffs on products of China with an annual trade value of approximately $300 billion which is referred to as List 4 (or Tranche 4). The tariff subheadings subject to additional duties under Tranche 4 are separated into two lists (list 4a and 4b) with different effective dates listed below.

On August 30, 2019, the USTR published their determination to modify the action being taken in the Section 301 investigation by increasing the rate of additional duty from 10 to 15 percent for the products of China covered by the $300 billion tariff action (List 4). See 84 FR 45821.

- List 1 will be in effect on September 1, 2019 with additional duty of 15 percent

- List 2 will be in effect on December 15, 2019 with additional duty of 15 percent

Guidance

Products Covered by Tranche 4, Annex A (Described in Annex B) – additional duty of 15 percent ad valorem is effective September 1, 2019

The additional import duties for Chinese goods covered by Annex A, published in the August 20, 2019 list of products subject to the Section 301 action, and are effective with respect to goods entered, or withdrawn from warehouse for consumption, on or after 12:01 AM eastern daylight time on September 1, 2019. Any article classified in a subheading covered by Annex A that is a product of China is subject to a 15% ad valorem duty rate, in addition to the general (Column 1) rate of duty for that particular subheading. Therefore, in addition to regular chapter reporting requirements, report the following HTS number and duty rate.

|

HTS Duty Rate 9903.88.15 15 percent |

Products Covered by Tranche 4, Annex C (Described in Annex D) –additional duty of 15 percent ad valorem is effective December 15, 2019

The additional import duties for Chinese goods covered by Annex C, published in the August 20, 2019 list of products subject to the Section 301 action, are effective with respect to goods entered, or withdrawn from warehouse for consumption, on or after 12:01 AM eastern daylight time on December 15, 2019. Any article classified in a subheading covered by Annex C that is a product of China is subject to a 15% ad valorem duty rate, in addition to the general (Column 1) rate of duty for that particular subheading. Therefore, in addition to regular chapter reporting requirements, report the following HTS number and duty rate.

| HTS Duty Rate

9903.88.16 15 percent |

All Products Covered by Section 301 Duties and Chapter 98 and 99 Instructions

The Section 301 duties only apply to products of China, and are based on the country of origin, not country of export. Please refer to CSMS 18-000624 for Chapter 98 and 99 filing instructions.

Trade Preference Programs & Temporary Reductions in Rates of Duty

Products of China that are covered by the Section 301 remedy and that are eligible for special tariff treatment under general note 3(c)(i) to the tariff schedule, or that are eligible for temporary duty exemptions or reductions under subchapter II to chapter 99, shall be subject to the additional duty imposed by headings 9903.88.01, 9903.88.02, 9903.88.03, 9903.88.04, 9903.88.09, 9903.88.15, and 9903.88.16.

Foreign Trade Zones

Any product listed in Annex A, except any product that is eligible for admission under ‘domestic status’ as defined in 19 CFR 146.43, which is subject to the additional duty imposed by this determination, and that is admitted into a U.S. foreign trade zone on or after 12:01 am eastern daylight time on September 1, 2019, only may be admitted as ‘privileged foreign status’ as defined in 19 CFR 146.41. Such products will be subject upon entry for consumption to any ad valorem rates of duty or quantitative limitations related to the classification under the applicable HTSUS subheading.

Any product listed in Annex C, except any product that is eligible for admission under ‘domestic status’ as defined in 19 CFR 146.43, which is subject to the additional duty imposed by this determination, and that is admitted into a U.S. foreign trade zone on or after 12:01 am eastern daylight time on December 15, 2019, only may be admitted as ‘privileged foreign status’ as defined in 19 CFR 146.41. Such products will be subject upon entry for consumption to any ad valorem rates of duty or quantitative limitations related to the classification under the applicable HTSUS subheading.

Duty Drawback

Section 301 duties are eligible for duty drawback. What is Duty Drawback? Do you currently claim it? If the answer is no, you may be leaving money on the table. Duty drawback allows an organization to obtain a refund for paid Customs duties on imported products or U.S.-manufactured products with imported components that have been exported back out of the United States. Importers can receive up to 99% of their previously paid duties. There is a one time opportunity for a shipper to claim drawback up to five retroactive years. To learn if your company qualifies, send an email to consulting@scarbrough-intl.com to set up a 20-minute free consultation.

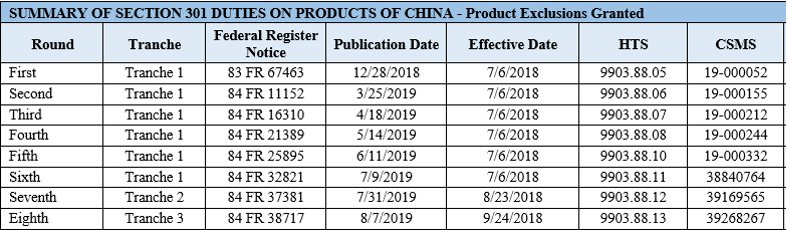

Product Exclusions

The USTR will establish a process by which interested persons may request that particular products classified within an HTSUS subheading covered by Annex A and Annex C may be excluded from the additional duties. USTR will publish a separate notice describing the product exclusion process, including the procedures for submitting exclusion requests, and an opportunity for interested persons to submit oppositions to a request. CBP will also provide additional guidance on the matter as it becomes available.

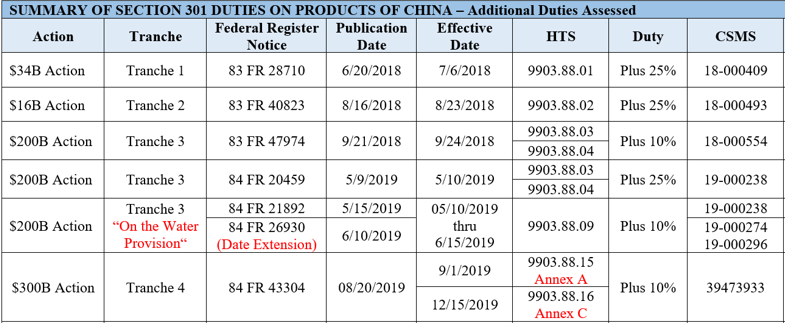

For ease of reference, Summaries of Section 301 Duties and Product Exclusion Notifications are provided in the tables below. Detailed information about a specific Tranche or Product Exclusion Round may be obtained from any of the source documents listed.

To learn if your company qualifies for an exclusion or you need help filing for exclusions or receiving a refund from CBP, send an email to consulting@scarbrough-intl.com to set up a 20-minute free consultation. View details on Section 301 Product Exclusions here.

More Information from CBP

For more information related to Tranche 4 additional duties imposed on the tariff subheadings set out in Annex A/B and Annex C/D, please refer to 84 FR 43304, issued August 20, 2019 and 84 FR 45821, issued August 30, 2019. More information may also be found at https://www.cbp.gov/trade/remedies.

Related CSMS Messages

Insert this exact phrase in the search bar: 18-000409, 18-000493, 18-000554, 19-000238, 19-000274, 19-000296, 19-000052, 19-000155, 19-000212, 19-000244, 19-000332, 38840764, 39169565, 39268267, 39473933

Duty Savings

If the Section 301 tariffs are affecting your company, watch this webinar recording to learn more. Scarbrough’s President and COO, Adam Hill, along with Patrick Caulfield, an attorney at GDLSK, an international trade and customs law firm, talk about legal opportunities to recover or avoid paying duty to CBP.

Consulting

Scarbrough is offering a FREE 20-minute consultation to any importer affected by the Section 301 Tariffs. Email consulting@scarbrough-intl.com or fill out the form below.

Oops! We could not locate your form.

To review Section 301, visit this helpful Resource Page

To read more about Section 301, visit USTR.gov